Introduction

Commercial real estate closing costs have a way of catching buyers off guard — not because they're hidden, but because most buyers don't model them until it's too late to do anything about them.

Unlike a home purchase, a commercial closing in Florida layers lender requirements, environmental investigations, specialized surveys, and Florida-specific transfer taxes on top of the standard title and escrow work. Buyers who have closed residential deals before often assume the process is similar. It isn't.

According to a GlobeSt report on rising transaction costs in commercial real estate, legal fees alone are becoming a meaningful cost driver in CRE deals. That's before factoring in Florida's documentary stamp taxes, ALTA surveys, Phase I environmental reports, and lender-mandated appraisals.

This guide breaks down what commercial closing costs consist of in Florida, what drives them up or down, who typically pays what, and how to build a realistic closing budget before you reach closing.

Key Takeaways

- Florida commercial closing costs vary by property type, financing structure, and county.

- Costs fall into five buckets: lender fees, title and escrow, due diligence, legal and recording, and Florida taxes.

- Florida's documentary stamp taxes apply to both the deed and the mortgage, which catches many out-of-state buyers off guard.

- Buyers carry financing and due diligence costs; sellers carry disposition costs.

- Title insurance payment customs vary by county, so confirm local norms before making an offer.

How Much Do Commercial Real Estate Closing Costs Run in Florida?

Commercial closing costs don't have a fixed price tag. They shift based on purchase price, property type, loan structure, county, and how complex the title and due diligence work turns out to be. A straightforward cash purchase of an industrial building closes differently than a financed multi-tenant retail acquisition with environmental questions.

What's consistent is that buyers who underestimate these costs tend to face one of three problems:

- A cash shortfall at the closing table

- Return projections built on incomplete acquisition numbers

- Lost negotiating leverage because they didn't know which costs were shiftable

Understanding what drives costs at each deal size helps you build a realistic budget before you're at the closing table. Here's how the numbers typically break down.

Small Commercial Deals (Under $1M)

Buyers in this range sometimes assume costs will scale down proportionally. They don't. Title work, ALTA surveys, Phase I environmental assessments, and Florida's documentary stamp taxes are driven by scope and statute, not by a percentage of the purchase price.

A $700,000 industrial purchase can carry the same environmental and survey costs as a $2 million deal. The fixed components don't compress just because the property is smaller.

Mid-Size Deals ($1M–$5M)

This is where lender underwriting requirements add meaningful cost. Commercial appraisals at this tier are more complex than residential ones — they factor in the property's income approach and local market comparables. Environmental reports, ALTA/NSPS surveys (updated to the 2026 standards effective February 23, 2026), and lender-required third-party reports all arrive during the contract period — before you own anything.

Florida's documentary stamp and intangible taxes on the mortgage become a noticeable line item here. On a $3 million loan, those taxes combined run approximately $16,500 — a number that changes your cash-to-close figure materially if it's not budgeted early.

Large Transactions ($5M+)

Percentage ranges may compress slightly at higher deal values, but absolute dollar amounts grow fast. Florida's deed documentary stamp tax alone on a $5 million purchase runs $35,000 in most counties — or $52,500 in Miami-Dade for nonresidential transfers. Multi-tenant properties, complex title histories, and higher lender scrutiny all expand the cost file.

| Category | Included in These Ranges | Not Included |

|---|---|---|

| Lender fees | ✓ | |

| Title and escrow | ✓ | |

| Due diligence reports | ✓ | |

| Florida transfer taxes | ✓ | |

| Recording charges | ✓ | |

| Down payment | ✓ | |

| Post-closing capital improvements | ✓ | |

| Buyer-side brokerage commissions | ✓ |

Complete Cost Breakdown: What Goes Into a Florida Commercial Closing

The settlement statement is built from five distinct cost centers. Knowing what each one covers — before the numbers arrive — lets you budget accurately and negotiate from an informed position.

Lender Fees

Lender fees depend on the loan type (bank, SBA, private), the property's complexity, and the lender's internal processing structure. What falls into this category:

- Origination and underwriting fees — charged as a percentage of the loan or as a flat fee

- Commercial appraisal — more complex than residential, requiring income approach analysis, market comparables, and lender-specific documentation; cost drivers include property type, size, special-use features, and SBA documentation requirements

- Loan processing and document preparation fees

- Lender-mandated third-party reports — environmental review, property condition assessments, and sometimes zoning reports, depending on property type and lender requirements

SBA 7(a) and 504 loans carry their own appraisal and environmental standards governed by SBA SOP 50 10. Bank and private lenders set their own requirements, which vary considerably.

Title and Escrow Costs

Commercial title work takes longer and digs deeper than a residential title search. Prior liens, unreleased mortgages, easements, use restrictions, access questions, and recorded instruments affecting the property's usability all need to be surfaced and resolved before closing. Title and escrow costs cover:

- Title search and examination fees

- Owner's title insurance policy premium

- Lender's title insurance policy premium (required by most lenders)

- Escrow/settlement fee — paid to the closing agent for managing document collection, funds disbursement, recording coordination, and proration calculations

Golm Law Firm provides title and escrow services for commercial closings throughout Florida, with Crystal D. Golm having personally closed hundreds of millions of dollars in commercial transactions across property types including office buildings, retail centers, apartment complexes, and triple-net lease deals.

Due Diligence Costs

These costs arrive during the contract period — before you own the property — and most are owed whether the deal closes or not. Three items drive this category:

Phase I Environmental Site Assessment (ESA) — conducted under ASTM E1527-21, the current standard (last updated December 21, 2021). The Phase I identifies Recognized Environmental Conditions (RECs) on the property. If RECs surface, a Phase II ESA involving soil or groundwater sampling is typically the next step.

Commercial property inspection — covers structural systems, roof, HVAC, ADA compliance, life safety systems, and parking. Pricing methodology varies: inspectors may charge by square footage, flat scope, or a percentage of property value, per CCPIA guidance.

ALTA/NSPS Land Title Survey — required by most lenders and title insurers to remove the general survey exception from the title policy. The 2026 ALTA/NSPS standards (effective February 23, 2026) govern these surveys; they go significantly beyond a standard boundary survey and provide lenders and title companies with the detail they need to rely on the survey in underwriting.

Legal and Recording Costs

Attorney fees in a commercial deal reflect transaction complexity, not just property value. A financed acquisition with tenant estoppels, zoning questions, or title curative work costs more to close than a straightforward cash sale. Recording charges cover the deed, mortgage, and related instruments filed in Florida's public records system.

Buyers should budget for their own legal representation separately from the closing agent fee — these are distinct functions.

Taxes and Insurance

Florida imposes documentary stamp taxes on both the deed and the mortgage — separate charges that add up quickly on commercial transactions. Beyond taxes, buyers need to budget for commercial property insurance at closing. Two points worth flagging:

- Lenders require evidence of coverage before funding — this isn't optional

- Depending on the asset's location and type, wind and flood coverage may be mandatory, which can significantly affect premium costs

Florida-Specific Rules That Change the Numbers

Florida imposes state transfer taxes that are fixed by statute — not negotiable. They're also frequently underweighted in early acquisition budgets. Two instruments trigger tax at closing: the deed and the mortgage.

Documentary Stamp Tax on the Deed

Florida Statute 201.02 imposes a documentary stamp tax on the deed at $0.70 per $100 of consideration in most Florida counties.

| Purchase Price | Doc Stamp Tax (Most Counties) |

|---|---|

| $1,000,000 | $7,000 |

| $2,000,000 | $14,000 |

| $5,000,000 | $35,000 |

Miami-Dade County operates under a different structure. The base rate drops to $0.60 per $100, but nonresidential transfers carry an additional surtax of $0.45 per $100, bringing the effective total to $1.05 per $100 — 50% higher than the rest of the state. A $2 million commercial purchase in Miami-Dade costs $21,000 in deed doc stamps versus $14,000 elsewhere.

Documentary Stamp Tax and Intangible Tax on the Mortgage

Financed deals face two additional Florida charges that don't apply to cash purchases:

- Documentary stamp tax on the mortgage/note: $0.35 per $100 of the loan amount

- Nonrecurring intangible personal property tax: $2.00 per $1,000 of principal

On a $1.5 million loan, these two items add up as follows:

| Tax | Calculation | Amount |

|---|---|---|

| Doc stamp on mortgage | $1,500,000 ÷ 100 × $0.35 | $5,250 |

| Intangible tax | $1,500,000 ÷ 1,000 × $2.00 | $3,000 |

| Combined | $8,250 |

That's $8,250 in Florida mortgage taxes on a single loan. The figures shift meaningfully as loan amounts change, so these should be modeled before you sign a letter of intent — not after.

Title Insurance County Customs in Florida

Unlike many states with uniform practice, Florida's title insurance payment customs vary by county — and the difference affects who controls title company selection.

According to Barnes Walker and Weston Title, county customs break down as follows:

- Manatee County: Seller customarily pays for owner's title insurance and selects the title company

- Sarasota County: Buyer customarily pays and selects the title company

- Hillsborough and Pinellas Counties: Seller customarily pays

These are customs, not legal requirements, and commercial contracts can and do deviate from them. The practical consequence is that buyers who don't know the local custom before making an offer may miscalculate their cash-to-close figures. Golm Law Firm, based in Bradenton, advises commercial buyers across Manatee and Sarasota Counties on which custom applies and whether the contract terms reflect it accurately.

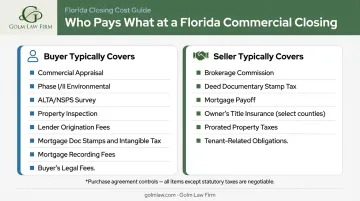

Buyer vs. Seller: Who Pays What in a Florida Commercial Deal

Cost allocation in commercial deals starts with custom — but the purchase and sale agreement ultimately controls who pays what. Buyers who negotiate cost allocation before signing can shift thousands of dollars in closing expenses.

Costs Buyers Typically Cover

- Commercial appraisal (lender-required)

- Phase I (and if triggered, Phase II) environmental assessment

- ALTA/NSPS survey

- Commercial property inspection

- Lender origination, underwriting, and processing fees

- Documentary stamp tax and intangible tax on the mortgage

- Recording fees for the mortgage

- Buyer's own legal fees

Any due diligence the buyer elects beyond lender minimums stays with the buyer unless the contract says otherwise.

Costs Sellers Typically Cover

- Brokerage commission — negotiable and not set by law; NAR confirms commissions are not mandated by any association or statute

- Documentary stamp tax on the deed

- Outstanding mortgage payoff

- Owner's title insurance and title search (in counties where seller custom applies)

- Prorated property taxes

- Tenant-related obligations (estoppel certificate procurement, lease assignment fees)

When brokerage commission is included, seller closing costs can represent a meaningful slice of gross sale proceeds. That's reason enough for sellers to have their own attorney reviewing the final settlement statement.

What Is Negotiable

Everything beyond Florida's statutory tax rates is negotiable:

- Title insurance responsibility (flipping the custom)

- Seller credits toward buyer closing costs

- Survey cost sharing or use of an existing seller survey

- Curative title work costs when the defect originates from the seller's chain of title

The best time to raise these points is at the letter-of-intent stage — before both parties have invested in due diligence and legal fees that make walking away costly.

How to Build and Protect Your Commercial Closing Budget in Florida

Commercial buyers who wait until after contract execution to calculate closing costs find their options already locked in. The time to shape those costs is before the ink dries — not after the lender has set conditions and the closing date is two weeks out.

Negotiate Before the File Gets Expensive

At the LOI or early contract stage, three moves deliver the most value:

- Request seller credits toward defined closing costs as part of the economic package

- Push curative title costs (expenses to fix title defects) to the seller when the defect originates from their side of the ownership history

- Ask whether the seller has a recent usable survey or existing third-party reports — reusing them (with lender approval) avoids duplication

Once the title commitment is issued, the lender has set conditions, and the closing date is approaching, flexibility shrinks fast.

Build the Budget Into Your Underwriting from Day One

Four items that commercial buyers routinely underestimate:

- Doc stamp and intangible taxes on the mortgage — fixed by statute and invisible until the settlement statement arrives

- County-specific title insurance customs — affects who controls title selection and who pays

- Due diligence costs owed even if the deal falls through — environmental reports, surveys, and inspections don't come back if the contract terminates

- Lender-required third-party reports that expand by property type — a gas station, a school, or a property with prior industrial use triggers more extensive environmental inquiry than a suburban office building

Buyers who model these into their initial pro forma close with fewer surprises and stronger negotiating positions than those who calculate them at the end.

Review the Settlement Statement Like a Deal Document

That same discipline carries through to the closing table. Before wires go out, review the settlement statement line by line. Look for:

- Duplicative charges from multiple service providers

- Unclear or unexplained lender fees

- Proration errors on rent, taxes, or utilities

- Tax calculations that don't match the statutory rates

Errors found at this stage are negotiable. Errors missed after wires go out are not.

Conclusion

Commercial real estate closing costs in Florida are a real and substantial part of the acquisition cost. The five cost categories — lender fees, title and escrow, due diligence, legal and recording, and Florida taxes — each carry line items that compound quickly, particularly when Florida's documentary stamp taxes on both the deed and the mortgage are factored in.

Buyers who map out these costs before the purchase and sale agreement is signed avoid the budget overruns that catch underprepared buyers at the closing table.

If you're preparing for a commercial purchase, contract review, or closing in Florida, engaging an experienced commercial real estate attorney before the PSA is finalized is the clearest way to protect your budget and avoid costly surprises.

Golm Law Firm has closed hundreds of millions of dollars in commercial real estate transactions across Florida — office buildings, retail centers, apartment complexes, and triple-net lease deals — and provides the transaction-specific guidance that commercial buyers in Manatee, Sarasota, and throughout Florida need to reach closing on budget.

Frequently Asked Questions

What are typical closing costs on a commercial property?

Commercial closing costs typically run 2%–5% of the purchase price nationally, but Florida's deed doc stamps, mortgage doc stamps, and intangible tax push financed deals toward the higher end. On a $2 million financed purchase, total costs can reach $60,000–$100,000 or more depending on loan size and property complexity.

What are typical buyer closing costs in Florida for commercial real estate?

Buyers primarily cover lender fees, due diligence costs (environmental assessment, ALTA survey, inspection), mortgage doc stamps and intangible tax, recording fees, and legal costs. Note that many of these — especially due diligence reports — are due during the contract period, not only at closing.

Who typically pays closing costs on commercial real estate in Florida?

Buyers typically cover financing and investigative costs; sellers typically cover disposition costs including brokerage commission and documentary stamp tax on the deed. However, state law doesn't mandate this split — the purchase and sale agreement controls the allocation, and both parties can negotiate different terms.

Are commercial real estate closing costs higher than residential in Florida?

Commercial closings carry cost layers residential transactions don't: Phase I environmental assessments, ALTA/NSPS surveys, commercial appraisals, property condition assessments, and lender-required third-party reports. Florida's mortgage doc stamp tax adds further cost on financed deals — making commercial closings noticeably more expensive than residential deals at the same price point.

Can commercial real estate closing costs be negotiated in Florida?

Yes — title insurance responsibility, seller credits, survey cost sharing, and curative title work are all commonly negotiated in Florida commercial contracts. Cost allocation discussions are most productive at the letter-of-intent stage, before due diligence and legal spend make both parties reluctant to walk away.

What Florida-specific taxes apply at a commercial real estate closing?

Three main items: documentary stamp tax on the deed ($0.70 per $100 of purchase price in most counties), documentary stamp tax on the mortgage ($0.35 per $100 of loan amount), and nonrecurring intangible tax on the mortgage ($2.00 per $1,000 of principal). Miami-Dade County adds a nonresidential surtax on the deed, bringing that county's total deed tax to $1.05 per $100 — 50% higher than the rest of the state.