Introduction

Falling behind on mortgage payments in Florida puts homeowners in a difficult position. A judicial foreclosure is a public court process that can stretch well over a year, creating real financial and emotional pressure. For some homeowners, a deed in lieu of foreclosure offers a way out: transfer the property directly to the lender, satisfy the debt, and skip the formal foreclosure entirely.

A deed in lieu is not a clean escape by default, though. Florida law creates specific risks around deficiency judgments, documentary stamp tax, and junior liens that many homeowners don't see coming until it's too late. Whether this option works in your favor depends almost entirely on what the agreement actually says — and whether you had qualified legal review before signing.

This article breaks down both sides, covering the actual pros, the overlooked risks, and what Florida law requires.

Key Takeaways

- Transfers property ownership voluntarily to the lender, bypassing formal foreclosure proceedings

- Potential benefits include avoiding a lengthy public court process and negotiating a deficiency waiver

- Junior liens survive a deed in lieu and are not extinguished — a critical distinction from judicial foreclosure

- Florida Statute §702.06 allows deficiency claims unless the deed in lieu agreement explicitly waives them

- Forgiven debt may be taxable income — consult a tax professional before signing

What Is a Deed in Lieu of Foreclosure in Florida?

What Is a Deed in Deed in Lieu of Foreclosure in Florida?

A deed in lieu of foreclosure is a voluntary agreement where a homeowner transfers the property's title directly to the lender in exchange for cancellation of the mortgage debt. The homeowner hands over the deed, and the lender agrees — in writing, if negotiated correctly — to release the remaining debt. No auction, no sheriff's sale required.

Why Florida's Foreclosure Process Makes This Relevant

Florida is a judicial foreclosure state under Fla. Stat. §702.01, meaning every mortgage foreclosure must go through the court system. National data from ATTOM shows average foreclosure completion times of 577 days nationally in Q1 2026. Court filings, auction notices, and case records all become part of the public record under Florida Rule 2.420. For homeowners who want a defined exit with less public exposure, a deed in lieu has obvious appeal.

What a Deed in Lieu Is NOT

Before pursuing this route, understand what the process actually requires:

- Lender approval is required — homeowners cannot force acceptance

- The property typically needs clear title with no junior liens on the property

- Most lenders require the borrower to first attempt a loan modification or short sale

- Approval is not guaranteed and can take months

Understanding these limitations upfront helps homeowners decide whether pursuing a deed in lieu is worth the time and negotiation — or whether another exit strategy fits their situation better.

Pros of a Deed in Lieu of Foreclosure in Florida

The benefits below are real — but each one depends on what the agreement actually says. An unreviewed agreement may not deliver any of them.

Avoids a Lengthy, Public Foreclosure Process

Florida foreclosures move through the court system, and proceedings are part of the public record. Court filings, hearing dates, and auction notices can all be accessed by anyone. A deed in lieu sidesteps this entirely: no formal case, no public sale, no auction notice in the local paper.

The timeline difference is also significant. Judicial foreclosure can take well over a year. A deed in lieu, once the lender agrees to pursue it, can close in weeks to months. For homeowners who want a defined end date rather than an indefinite legal proceeding hanging over them, that difference matters.

May Eliminate the Remaining Mortgage Balance

When negotiated correctly, the deed in lieu agreement includes a full deficiency waiver — the lender releases the borrower from any remaining debt after the property's value is applied to the mortgage balance.

This matters because under §702.06, Florida lenders retain the right to sue for the deficiency even after accepting a deed in lieu — unless the agreement explicitly waives it. That waiver must be in writing. Verbal assurances mean nothing.

Florida Statute §95.11 provides a 1-year statute of limitations for residential mortgage deficiency claims after a deed in lieu is accepted, so lenders can still act on that right for a full year after the transaction closes.

Less Severe Credit Impact Than Foreclosure

A deed in lieu will damage your credit — no avoiding that. According to Experian, it can be reported as closed but not paid as agreed and may remain on your credit report for up to 7 years.

The distinction versus a completed foreclosure matters most for future mortgage eligibility:

| Event | Fannie Mae Waiting Period | Freddie Mac Waiting Period |

|---|---|---|

| Deed in lieu | 4 years (2 with extenuating circumstances) | 48 months (24 with extenuating circumstances) |

| Foreclosure | 7 years (3 with extenuating circumstances) | 84 months (36 with extenuating circumstances) |

Negotiating how the lender reports the event can also make a difference. Ask for "deed in lieu" rather than "foreclosure" in the credit reporting language — and get it in writing.

Potential Relocation Assistance ("Cash for Keys")

Some lenders offer relocation assistance: cash in exchange for vacating the property promptly and leaving it in good condition. This is sometimes called "cash for keys," and it's not guaranteed.

Under Fannie Mae guidelines, subordinate lien payoffs are capped at an aggregate $6,000 — a figure that reflects how limited lender flexibility tends to be in these transactions. If you're pursuing a deed in lieu, address relocation assistance directly during negotiations:

- Ask about cash-for-keys availability upfront

- Confirm the specific dollar amount in writing

- Get the conditions for payment documented in the agreement

Cons and Risks of a Deed in Lieu of Foreclosure in Florida

A deed in lieu is not a clean slate. Several significant risks can surprise Florida homeowners who proceed without legal guidance.

Junior Liens Survive the Transfer

This is the issue that kills most deed in lieu transactions before they start.

In a judicial foreclosure, junior lienholders named and served in the action have their interests extinguished through the court process. A deed in lieu does not work that way.

Junior liens — second mortgages, HOA liens, judgment liens — survive and remain attached to the property. The lender receiving the deed inherits title with those encumbrances still on it.

This creates two real problems:

- The lender may refuse to accept the deed in lieu because title isn't clean

- The borrower may still face collection from junior lienholders after the transaction

Title insurance companies may also decline to insure the lender's newly acquired property if subordinate liens remain — yet another reason lenders are selective.

Potential Tax Consequences

Any debt forgiven through a deed in lieu may qualify as cancellation of debt (COD) income under IRS rules, and according to IRS Topic 431, canceled debt is generally taxable and must be included in gross income unless an exclusion applies. Consult a tax professional before finalizing any deed in lieu agreement to determine which exclusion, if any, applies to your situation.

Potential exclusions include:

- Insolvency exclusion — if your liabilities exceeded your assets at the time of cancellation

- Qualified principal residence exclusion — applies to discharges before January 1, 2026, or under written arrangements entered before that date

Florida has no state income tax on individuals (Florida Constitution, Article VII, §5), so the liability is federal only. But it can be substantial.

Documentary Stamp Tax

Florida imposes documentary stamp tax under §201.02 on deeds transferring real property. The Florida Department of Revenue explicitly lists deeds in lieu of foreclosure as taxable documents. The rate is $0.70 per $100 of consideration statewide, with Miami-Dade County using different rates.

"Consideration" includes the amount of any mortgage or lien being discharged — meaning the tax is calculated on the mortgage balance, not just cash paid. On a $300,000 mortgage, that's $2,100 in documentary stamp tax alone. Most homeowners don't budget for this cost.

Lenders Are Not Required to Accept

The CFPB frames a deed in lieu as an option that "may" be available — not as a borrower's right. Lenders decline frequently, particularly when:

- Junior liens complicate the title

- The property is in poor condition

- The lender believes a short sale will yield a better return

- The borrower hasn't attempted a short sale first

Freddie Mac's guidelines specifically require servicers to evaluate deed in lieu only after home-retention options and standard short sale options are determined not viable. Understanding these requirements upfront — and having legal counsel review your situation before you approach the lender — reduces the risk of a rejected application and wasted time.

What Florida Law Says About Deed in Lieu Agreements

No single Florida statute governs deed in lieu transactions as a whole, but several statutes directly shape the outcome:

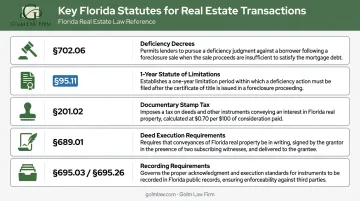

- §702.06 — Governs deficiency decrees. Explicitly addresses deed-in-lieu deficiency calculations and caps the deficiency at the difference between the total debt and the property's fair market value on the date of transfer. Without a written waiver, the lender can still sue.

- §95.11 — Establishes a 1-year statute of limitations for residential mortgage deficiency claims following a deed in lieu. The clock starts the day after the mortgagee accepts the deed.

- §201.02 — Imposes documentary stamp tax on the deed transfer, calculated on the mortgage balance.

- §689.01 — Requires real estate conveyances to be in writing and signed in the presence of two subscribing witnesses.

- §695.03 and §695.26 — Set acknowledgment and recording requirements for the deed to be recorded in Florida.

What the Agreement Must Include

A valid, protective deed in lieu in Florida requires:

- A properly executed and recorded deed, signed before two witnesses, acknowledged, and satisfying Florida's recording requirements under §695.03 and §695.26

- A release or satisfaction of the mortgage that confirms the lender has fully relinquished its security interest in the property

- Explicit deficiency language — either a written waiver or an unambiguous statement of what the borrower still owes

If any of these elements is missing or poorly drafted, a borrower may face a deficiency lawsuit months after the transfer — on a debt they believed was settled. Before signing anything, have an attorney review every document in the package, not just the deed itself.

How to Navigate the Process and When to Get Legal Help

General Steps for Pursuing a Deed in Lieu in Florida

- Contact the lender or servicer — Request formal consideration and ask about their specific requirements

- Gather documentation — Hardship letter, income/expense documentation, property condition information, and a title report

- Negotiate the agreement terms — Deficiency waiver, relocation assistance, timeline to vacate, and credit reporting language

- Execute and record the deed — Following Florida's requirements under §689.01 and §695.03

Why Legal Review Is Not Optional

The agreement's language determines whether you escape the deficiency, avoid unexpected tax exposure, and get fair credit reporting. A lender's standard deed in lieu agreement is drafted to protect the lender — not you.

Golm Law Firm's attorneys assist Florida property owners in navigating deed in lieu negotiations, reviewing agreements for deficiency waiver language, identifying title complications, and ensuring all documentation is properly executed before anything is signed.

Crystal D. Golm has facilitated thousands of real estate transactions across Florida and understands how these agreements play out in practice. A 60-minute consultation with document review ($350) is a good place to start if you have an agreement in hand.

If the Deed in Lieu Falls Through

If the lender declines — or if junior liens make the transaction impractical — other options remain:

| Alternative | Key Consideration |

|---|---|

| Short sale | Sells to a third party; lender-approved; often required before deed in lieu |

| Loan modification | Restructures loan terms; keeps you in the property |

| Bankruptcy | May pause foreclosure proceedings; has significant long-term credit implications |

Frequently Asked Questions

Will I owe money after a deed in lieu of foreclosure?

Whether you owe money depends entirely on the deed in lieu agreement. Under §702.06, Florida lenders can still pursue a deficiency judgment for the shortfall between the mortgage balance and the property's fair market value. That right only disappears if the agreement explicitly waives it in writing. Never assume the debt is gone without seeing that language in the document.

Who accepts a deed in lieu of foreclosure?

The lender or mortgage servicer must accept — and they are not required to. Lenders typically require clear title with no junior liens, a property in reasonable condition, documented financial hardship, and evidence that other options like a short sale were attempted first.

How does a deed in lieu of foreclosure affect my credit score?

A deed in lieu stays on your credit report for up to 7 years, reported as closed but not paid as agreed. The mortgage waiting period is shorter than a completed foreclosure — 4 years vs. 7 years for Fannie Mae loans. Negotiating the credit reporting language with your lender upfront can reduce the long-term impact.

What are the tax consequences of a deed in lieu of foreclosure in Florida?

Forgiven debt may be treated as cancellation of debt income under IRS rules and could be taxable at the federal level. Exclusions exist — such as the insolvency exclusion and the qualified principal residence exclusion (for discharges before January 1, 2026) — but none apply automatically. Consult a tax professional before signing.

What happens to junior liens in a deed in lieu of foreclosure in Florida?

Junior liens — second mortgages, HOA liens, judgment liens — survive a deed in lieu and are not extinguished. Unlike a judicial foreclosure, where named junior lienholders lose their interests through the court process, a deed in lieu leaves those claims intact. Surviving junior liens frequently cause lenders to reject deed in lieu requests outright.

How is a deed in lieu different from a short sale in Florida?

In a short sale, the homeowner sells the property to a third-party buyer for less than the mortgage balance with lender approval. In a deed in lieu, the property transfers directly to the lender. Most lenders require a short sale attempt before considering a deed in lieu, and short sales can offer more flexibility in negotiating credit reporting terms.